Dennis Holmquist

612-867-7636

MENU

MENU

Home

Property Search

Listings

Resources

Sellers

Buyers

News

About

Contact

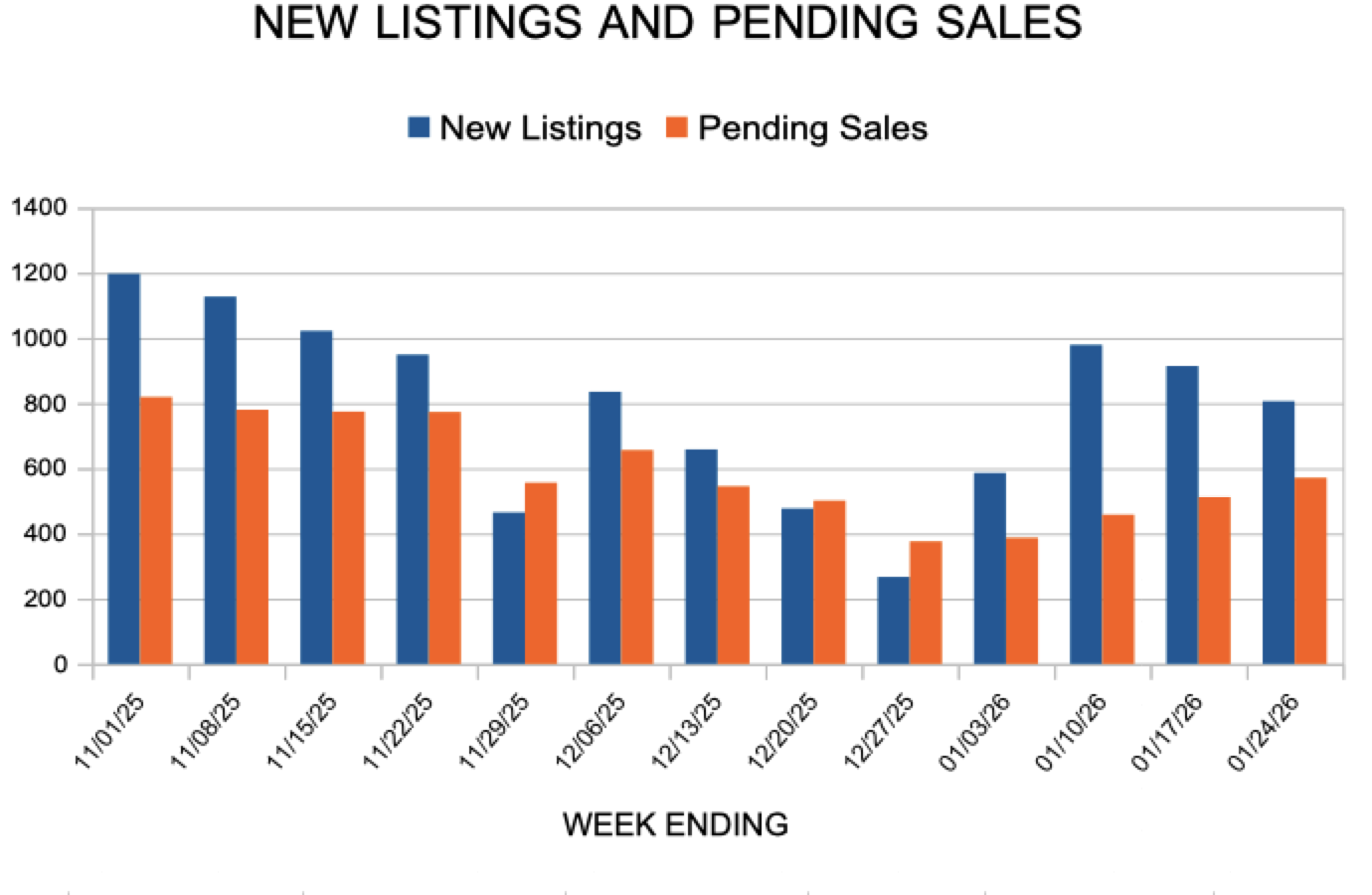

New Listings and Pending Sales

April 2, 2026

by

New Listings and Pending Sales

March 2, 2026

by

New Listings and Pending Sales

February 2, 2026

by

Leave a Comment

New Listings and Pending Sales

February 2, 2026

by

Leave a Comment

New Listings and Pending Sales

February 2, 2026

by

Leave a Comment

New Listings and Pending Sales

February 2, 2026

by

Leave a Comment

New Listings and Pending Sales

February 2, 2026

by

Leave a Comment

New Listings and Pending Sales

February 2, 2026

by

Leave a Comment

New Listings and Pending Sales

February 2, 2026

by

Leave a Comment

New Listings and Pending Sales

February 2, 2026

by

Leave a Comment

1

2

3

…

26

Next Page »